Partnerships Granted Limited Relief on Providing Part IV Information on Form 8308 to Partners for 2023 Tax Year

In Notice 2024-19, the IRS has offered relief to partnerships mandated to disclose extra information on Form 8308. This pertains to the sales or exchanges of partnership interests under the “hot asset” provisions of IRC §751(a).

The Notice begins:

This notice provides relief from penalties under § 6722 of the Internal Revenue Code1 for failures to furnish correct payee statements solely for failure of a partnership with unrealized receivables or inventory items described in § 751(a) (§ 751 property) to furnish Part IV of Form 8308, Report of a Sale or Exchange of Certain Partnership Interests, to the transferor and transferee in a § 751(a) exchange (described in section II of this notice) that occurred in calendar year 2023 by the due date specified in § 1.6050K-1(c)(1). This relief applies only if the partnership furnishes to the transferor and transferee by the due dates specified in section III of this notice (1) a correct copy of Parts I, II, and III of Form 8308, or a statement that includes the same information, and (2) a correct copy of the complete Form 8308, including Part IV, or a statement that includes the same information and any additional information required under § 1.6050K-1(c).

Form 8308 Requirements

Section II of the Notice details the filing requirements for Form 8308 that were in place prior to the 2023 tax year.

Generally, § 6050K and § 1.6050K-1 require a partnership with § 751 property to provide information to each transferor and transferee that are parties to a sale or exchange of an interest in the partnership (or portion thereof) in which any money or other property received by a transferor from a transferee in exchange for all or part of the transferor’s interest in the partnership is attributable to § 751 property (§ 751(a) exchange). Section 1.6050K-1(a)(2) provides that partnerships are required to report each § 751(a) exchange on Form 8308. Generally, § 1.6050K-1(f)(1) provides that a partnership is required to file Form 8308 as an attachment to its Form 1065, U.S. Return of Partnership Income, for the taxable year of the partnership that includes the last day of the calendar year in which the § 751(a) exchange took place. Form 8308 is due at the time for filing the partnership return, including extensions.

In addition, § 1.6050K-1(c)(1) provides that each partnership that is required to file a Form 8308 must furnish a statement to the transferor and transferee by the later of (a) January 31 of the year following the calendar year in which the § 751(a) exchange occurred, or (b) 30 days after the partnership has received notice of the exchange as specified under § 6050K and § 1.6050K-1. A partnership must use a copy of the completed Form 8308 as the required statement unless the Form 8308 contains information for more than one § 751(a) exchange. Section 1.6050K-1(c)(1) provides that if the partnership does not use the Form 8308 as the required statement, the partnership must furnish a statement that includes the information required to be shown on the Form 8308 with respect to the § 751(a) exchange to which the person to whom the statement is furnished is a party.

Section 6722 imposes a penalty for failure to furnish correct payee statements on or before the required date, and for any failure to include all of the information required to be shown on the statement or the inclusion of incorrect information. For these purposes, payee statements include statements required to be furnished to transferors and transferees under § 6050K. See § 6724(d)(2)(P). Section 6724 provides an exception to the imposition of a penalty under § 6722 if it is shown that the failure is due to reasonable cause and not to willful neglect.

In 2022, the IRS updated the regulations, expanding the scope of information required on Form 8308 for these scenarios.

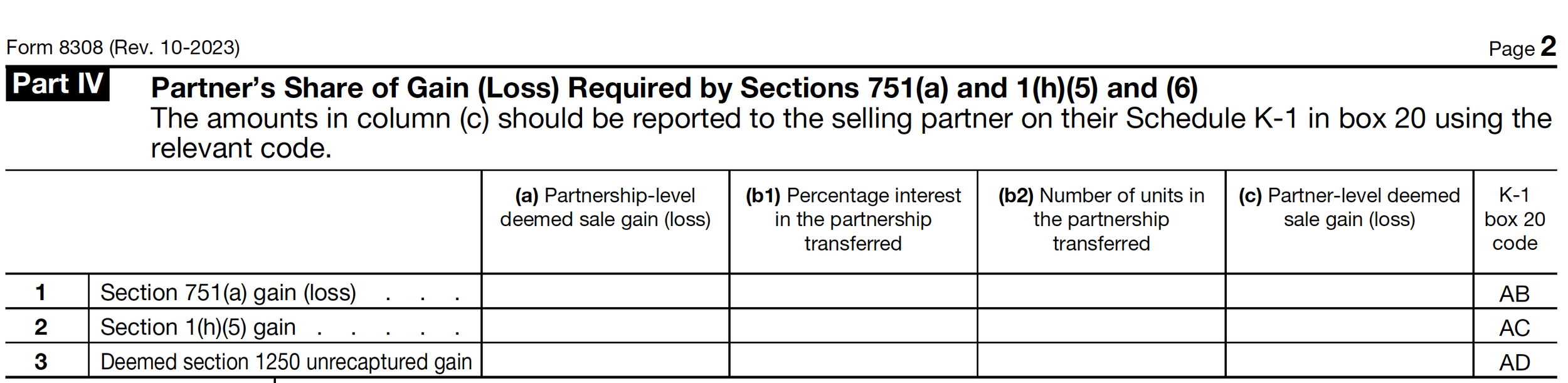

On November 30, 2020, the Department of the Treasury (Treasury Department) and the Internal Revenue Service (IRS) published T.D. 9926, 85 FR 76910, which amended § 1.6050K-1(c)(2) to require a partnership to furnish to a transferor partner the information necessary for the transferor to make the transferor partner’s required statement in § 1.751-1(a)(3). Among other items, § 1.751-1(a)(3) requires a transferor partner in a § 751(a) exchange to submit with the transferor partner’s income tax return a statement setting forth the amount of gain or loss attributable to § 751 property. In October 2023, the IRS released a revised version of Form 8308. Consistent with the requirements in § 1.6050K-1(c)(2), new Part IV of the 2023 Form 8308 requires a partnership to report, among other items, the partnership’s and the transferor partner’s share of § 751 gain and loss, collectibles gain under § 1(h)(5), and unrecaptured § 1250 gain under § 1(h)(6).

The supplementary information is detailed in Part IV of the updated Form 8308, which is dated October 2023.

In justifying the issuance of this Notice, the IRS acknowledges the numerous comments received, highlighting concerns that the information required for Part IV may not be available to many partnerships by January 31. The Notice further elaborates:

Since the issuance of the revised Form 8308, concerns have been expressed to the Treasury Department and the IRS that many partnerships will be unable to furnish the information required in Part IV of the 2023 Form 8308 to transferors and transferees by the January 31, 2024 due date, because, in many cases, partnerships will not have all of the information required by Part IV of the 2023 Form 8308 by January 31, 2024.

Relief Granted

Section III of the Notice outlines the following relief measures for partnerships that are unable to provide information to transferors and transferees by January 31, 2024:

With respect to § 751(a) exchanges during calendar year 2023, the IRS will not impose penalties under § 6722 solely for failure to furnish Form 8308 with a completed Part IV by the due date specified in § 1.6050K-1(c)(1) for a partnership that (1) timely and correctly furnishes to the transferor and transferee a copy of Parts I, II, and III of Form 8308, or a statement that includes the same information, by the later of (a) January 31, 2024, or (b) 30 days after the partnership is notified of the § 751(a) exchange, and (2) furnishes to the transferor and transferee a copy of the complete Form 8308, including Part IV, or a statement that includes the same information and any additional information required under § 1.6050K-1(c), by the later of (a) the due date of the partnership’s Form 1065 (including extensions), or (b) 30 days after the partnership is notified of the § 751(a) exchange.

The Notice further cautions that this relief does not extend to the obligation of filing Form 8308 with the partnership’s income tax return for the relevant tax year.

The relief provided in this notice applies only with respect to furnishing Form 8308 to the transferor and transferee. This notice does not provide relief with respect to filing Form 8308 as an attachment to a partnership’s Form 1065; as such, this notice does not provide relief from penalties under § 6721 for failure to file correct information returns.

What Will Happen for Future Years

This Notice is applicable solely to partnership income tax returns for the 2023 tax year. The future course of action by the IRS for subsequent tax years remains uncertain. The issue addressed by the IRS is not likely to diminish in future years, as it often seems improbable for partnerships to acquire all necessary information merely 31 days after the conclusion of the relevant year.